Summary

- As high inflation continues to reduce discretionary income for US consumers, dining out has become less affordable. US restaurant traffic has been declining for eight consecutive quarters, and pizza chains are also feeling the impact – as are producers of corrugated pizza boxes.

- However, demand for corrugated pizza boxes, which are only used for off-premise consumption, has been partially supported by an increasing shift from on-premise consumption to takeout and delivery. Still, overall demand for pizza boxes has been down from its pandemic peaks.

- Pizza boxes remain a crucial outlet for many corrugated producers, who are suffering from wider loss of demand across the board. Strength in delivery platforms may make up for some of the loss, but public pizza chain transactions and sales are still trending negative. We anticipate that pizza box demand will remain weak throughout 2025, given a gloomy economic outlook and shifting consumer preferences toward healthier and more globally diverse foodservice options. On a brighter note, opportunities are emerging for customized, short-run pizza boxes. Corrugated producers should focus on innovations that elevate the consumer experience.

Sustained traffic decline hits US pizza chains

The US economy is showing signs of deceleration, and consumers are becoming more cautious with their spending. While food categories – particularly those tied to at-home consumption – remain relatively resilient as essential goods, uncertainty persists around the outlook for foodservice demand. With shrinking discretionary income, consumers may reduce pizza orders, leading to a decline in pizza box usage.

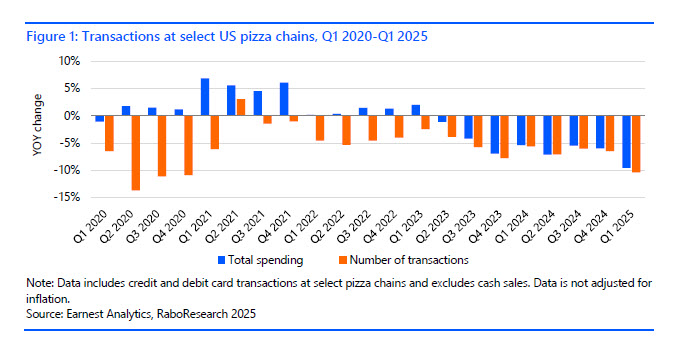

Indeed, US restaurants have been experiencing declining traffic and sales amid stagnant inflation, high interest rates, and tariff uncertainties. According to a recent RaboResearch report, Q1 2025 was the eighth quarter of consecutive traffic decline for US restaurant chains. The impact varied across different types of restaurants. Pizza chains, although not the hardest hit, saw a 10.4% YOY decline in transactions in Q1 2025 (see figure 1). This decline has progressively worsened since mid-2021. Overall sales have also weakened, which is particularly concerning given the 3.8% food- away-from-home inflation rate recorded in March 2025.

While this data encompasses both on-premise consumption and delivery/takeout orders paid in- store or directly through chains’ websites or mobile apps, we believe the significant decline is primarily driven by on-premise consumption. This is because dining-in sales account for the majority of transactions among the pizza chains included in this dataset.

Delivery keeps pizza chains afloat amid industry slump

Pizza delivery and takeout, the segment most relevant for corrugated box demand, also saw a decline in sales in recent quarters, though to a lesser extent. This was largely due to a shift in consumer behavior favoring more at-home food consumption over costlier on-premise dining. While this trend generally supports increased grocery purchases and home cooking, pizza remains a staple of restaurant delivery and takeout, offering an affordable and convenient option for feeding families or groups.

Recent results from publicly traded, delivery-focused pizza chains support this trend. While their year-over-year sales remain negative, they have been less impacted than the broader pizza restaurant category, which includes both on- and off-premise dining. Domino’s, the leading delivery-oriented chain in the US, reported a 2.4% YOY sales decline in Q1 2025 after adjusting for inflation – with sales essentially flat compared to Q1 2020. Papa Johns posted an inflation- adjusted year-on-year decline of 4.6% in Q1 2025, or 1.4% below Q1 2020 levels. In contrast, Pizza Hut, which relies more heavily on on-premise dining, experienced a sharp 10.4% YOY drop, translating to a 25.1% decline compared to Q1 2020.

While pizza delivery and takeout performed better than on-premise consumption, it also trended downward throughout 2024, mostly erasing the gains it saw during the Covid period. This decrease in pizza chain transactions and sales has led to a decline in pizza box demand.

Delivery platform strength is here to stay

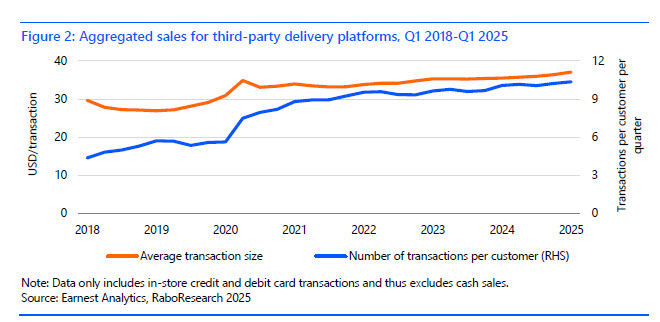

Delivery and takeout channels in the US experienced significant growth in 2020 during the early months of pandemic-induced restaurant closures and social distancing measures. This shift has had a lasting impact on consumer behavior, prompting foodservice operators of all sizes to invest in delivery and takeout infrastructure and technologies – investments that have largely remained in place even after Covid restrictions were lifted, as publicly announced by many US chains. We continue to observe growth in the number of transactions per customer on third-party delivery platforms across different cuisines, building on the surge that began in 2020 (see figure 2).

Additionally, the steady increase in average ticket size further underscores the strength and sustainability of the third-party delivery model.

Compared to pre-pandemic times, today’s consumers enjoy significantly greater access to online ordering across virtually all menu categories. This includes direct ordering through company- owned websites and mobile apps – primarily used by large chains with the resources to scale – as well as through third-party platforms like Uber Eats and DoorDash, which offer independent restaurants and smaller chains a fast, convenient way to reach customers, albeit for a fee.

Independent pizza restaurants, which represent roughly half of the US pizza market, can now compete more directly with large chains thanks to advancements in ordering technology and access to third-party delivery platforms. This shift helps offset some of the decline in pizza box demand from major chains as independents increasingly participate in the delivery and takeout economy.

Delivery apps open the door to global cuisines

However, while third-party apps support overall corrugated packaging demand, they also dilute pizza’s dominance as the go-to delivery item, thus reducing overall pizza box demand. These platforms expand consumer choices, making a wide variety of cuisines, such as Thai, Peruvian, or BBQ, just as accessible as pizza. When deciding what to order, especially in group settings, consumers may venture to explore diverse options. This trend is reinforced by a growing preference among US consumers for healthier and globally inspired menus, as highlighted in the RaboResearch report mentioned above.

Pizza boxes are a key part of corrugated demand

The ongoing weakness in US pizza chain performance is particularly concerning for corrugated producers with significant exposure to the pizza box segment. According to the American Forest and Paper Association (AF&PA), approximately 3 billion pizza boxes are used annually in the US. While pizza boxes represent a relatively small share of total corrugated demand, they can account for more than half of a converter’s volume in certain regions, depending on the local business mix. In areas with limited industrial manufacturing, pizza boxes serve as a critical source of corrugated packaging demand.

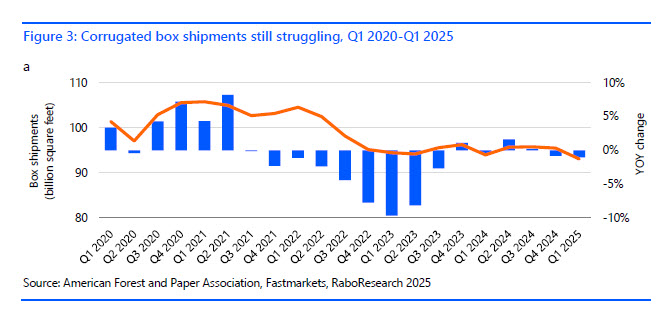

According to the latest data from AF&PA, overall corrugated box shipments declined by 1% YOY in Q1 2025, with kraftliner operating rates hovering around 85% (see figure 3). While operating rates aren’t as bad as in 2023, they reflect a continuous slowdown in corrugated demand across both industrial and retail sectors, driven in part by inventory buildups at box plants.

The outlook for pizza box demand

Delayed return to growth

With discretionary income under continued pressure, consumers are likely to remain cautious about dining out. Pizza delivery and takeout, often considered an affordable catering option, has traditionally been seen as somewhat recession resistant. However, several emerging factors could challenge this resilience:

- A peak in pizza delivery/takeout: Pizza saw exceptional growth during the pandemic, so the decline seen in the data may be due to the comparison to that strong period. Consumers may now be experiencing “pizza fatigue.”

- Health consciousness: Rising interest in wellness and anti-obesity drugs is steering consumers, especially from higher-income segments, toward perceived healthier (e.g., higher-protein, lower-calorie) options.

- Budget constraints: Cost-conscious consumers may trade down for more affordable options, opting for grocery stores’ frozen pizza instead of ordering out, though retail sales have yet to show a meaningful spike.

- Income divergence: Premium and health-focused food outlets are thriving, while segments targeting lower-income consumers, including quick-service restaurants, are seeing sharper declines.

These dynamics limit the potential of pizza delivery and takeout benefiting from a typical “recession trade-down” effect. As a result, category growth is likely to remain tied to broader macroeconomic trends. While rising incomes and low unemployment remain supportive, and inflation continues to ease gradually, recent volatility – particularly from newly imposed tariffs – has dampened consumer sentiment and may delay the anticipated foodservice recovery.

Therefore, we anticipate a delayed return to growth in pizza box demand, likely not materializing until late 2025 or into 2026. This recovery will depend on improved consumer sentiment, which currently sits at recession-like levels, as well as price stabilization and continued strength in incomes and employment. Pizza delivery and takeout remain well-positioned for a rebound and are likely to be among the first categories to benefit from a macroeconomic upturn. However, corrugated producers should prepare for continued softness in demand in the near term. This soft demand also limits the number of pizza boxes entering the recycling stream, which could further tighten the supply of old corrugated containers (OCC).

Packaging the new palate

Shifting consumer preferences toward more novel, global, and health-conscious options – such as salads and Mediterranean cuisine – have also impacted pizza demand. Additionally, advances in technology have made it easier for consumers to discover and order from smaller, independent pizza operators, further fragmenting the market.

We see two key strategies for pizza and pizza box producers to navigate these changes:

- Winning back value-driven consumers by leveraging deals and incorporating messaging on pizza boxes to reinforce the value proposition.

- Targeting more affluent segments through premium ingredients, innovative styles and toppings, and improved packaging that reflects the upgraded experience.

Looking beyond 2026, as the pizza segment continues to fragment amid the rise of smaller and premium formats, corrugated packaging producers will find increasing opportunities to meet demand for more customized, short-run box solutions. To stay competitive, producers should prioritize innovations that enhance both the consumer experience and specific-use occasions – such as Pizza Hut’s moving day campaign (with a pizza box that folds into a table).

Additionally, corrugated producers should explore packaging innovations beyond pizza boxes in faster-growing cuisines – such as multi-compartment solutions for Mediterranean meals – to unlock new growth avenues.

Report Authors

Xinnan Li

Senior Analyst – Packaging & Logistics

xinnan.li@rabobank.com

JP Frossard

Analyst – Consumer Foods

JP.Frossard@rabobank.com

Disclaimer

This document is meant exclusively for you and does not carry any right of publication or disclosure other than to Coöperatieve Rabobank U.A. (“Rabobank”), registered in Amsterdam. Neither this document nor any of its contents may be distributed, reproduced, or used for any other purpose without the prior written consent of Rabobank. The information in this document reflects prevailing market conditions and our judgement as of this date, all of which may be subject to change. This document is based on public information. The information and opinions contained in this document have been compiled or derived from sources believed to be reliable; however, Rabobank does not guarantee the correctness or completeness of this document, and does not accept any liability in this respect. The information and opinions contained in this document are indicative and for discussion purposes only. No rights may be derived from any potential offers, transactions, commercial ideas, et cetera contained in this document. This document does not constitute an offer, invitation, or recommendation. This document shall not form the basis of, or cannot be relied upon in connection with, any contract or commitment whatsoever. The information in this document is not intended, and may not be understood, as an advice (including, without limitation, an advice within the meaning of article 1:1 and article 4:23 of the Dutch Financial Supervision Act). This document is governed by Dutch law. The competent court in Amsterdam, the Netherlands has exclusive jurisdiction to settle any dispute which may arise out of, or in connection with, this document and/or any discussions or negotiations based on it. This report has been published in line with Rabobank’s long-term commitment to international food and agribusiness. It is one of a series of publications undertaken by the global department of RaboResearch Food & Agribusiness.

© 2025 – All rights reserved