US Power Market Outlook 2025-2030: Inside the Scramble to Meet Surging Power Demand

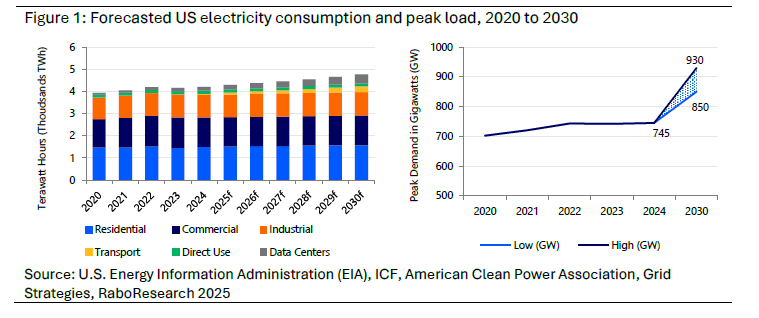

After two decades of flat growth, U.S. electricity demand is rising sharply. By 2030, consumption could jump 20%, with system peak load climbing from 745 GW today to as much as 930 GW (see figure 1). The surge is driven by data centers, electrification, and industrial onshoring—three forces that are adding continuous, geographically concentrated load faster than the grid was designed to handle. Peak demand is rising faster than average consumption because much of the new electricity use runs around the clock with little flexibility, creating localized stress on substations and transmission corridors even when national averages look manageable.

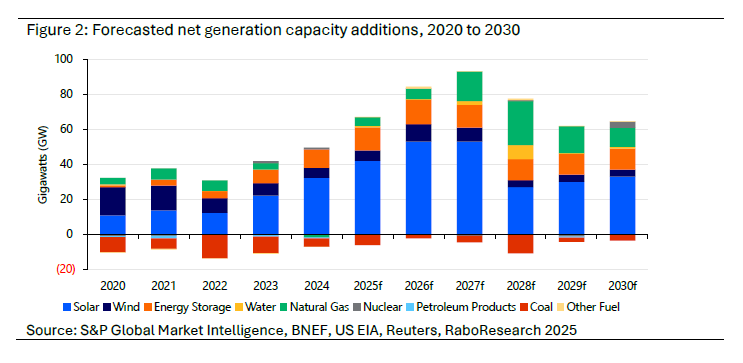

The supply response is visible but uneven. Renewables dominate near-term additions, with solar expected to add approximately 60 GW in both 2026 and in 2027, before moderating to around 30 GW thereafter. Storage maintains a steady 15 GW per year through 2030. Natural gas plants arrive late in the cycle, ramping to 17 GW annually between 2028 and 2030 as turbine manufacturing backlogs clear. Two factors explain this sequencing: economics and speed. Solar costs $38-78/MWh and can be built in 12-36 months. New combined-cycle gas plants cost $48-107/MWh on a levelized basis, but capital expenditures have surged from $722 million for a 1 GW plant in 2022 to $2.4 billion today, with projections reaching $2.8 billion by 2028 due to rapid demand growth, supply chain backlogs, and tariffs. Nuclear remains the most expensive option at $141-220/MWh, with timelines that stretch well beyond this decade.

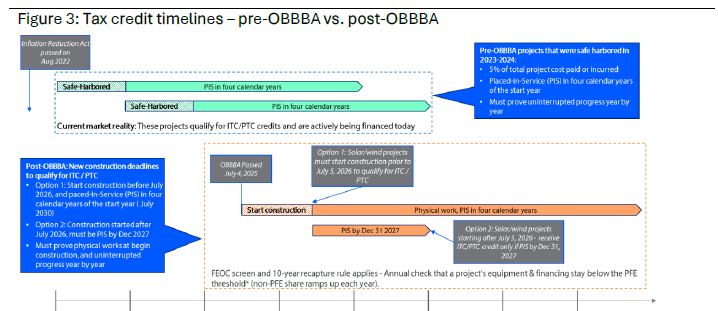

Policy is now the binding constraint. The One Big Beautiful Bill Act (OBBBA) compressed the tax credit qualification window. Projects that begin construction by July 4, 2026, are safe-harbored and eligible to receive full income tax credits (ITC) or production tax credit (PTC) credits under the four-year pathway. Those starting after must reach commercial operation by December 31, 2027 to qualify at all (see figure 3). Foreign Entity of Concern requirements add a decade of annual compliance reviews, with recapture provisions if supply chains fail to meet domestic content thresholds. Tariffs are compounding costs across all technologies, with storage hit hardest, up more than 60% on Chinese battery components. Pre-OBBBA projects that safe-harbored costs in 2023-2024 remain the most bankable, while post-OBBBA developers face tighter structuring and heightened diligence.

Source: Department of Commerce, Federal Register, US White House, RaboResearch 2025

The fuel dynamic is shifting as well. North American LNG export capacity is on track to more than double by 2028, from 11.4 bcf/d in 2023 to 24.4 bcf/d. US projects account for 9.7 bcf/d of that increase. As Gulf Coast liquefaction trains reach commercial operation, feed gas demand will climb, pulling supply from the same basins that serve power plants in gas-dependent markets. If scarcity develops, natural gas prices could rise. Combined with the elevated capital costs of new gas plants, this creates upward pressure on wholesale power prices and PPA rates. That raises a strategic question. If power prices drift higher due to LNG-linked gas costs and expensive dispatchable capacity, do renewables still need subsidies to compete? The answer will shape not just which projects get financed, but how much policy support is required to meet the demand growth now bearing down on the system.

Disclaimer

Disclaimer

This publication is issued by Coöperatieve Rabobank U.A., registered in Amsterdam, The Netherlands, and/or any one or more of its affiliates and related bodies corporate (jointly and individually: “Rabobank”). Coöperatieve Rabobank U.A. is authorised and regulated by De Nederlandsche Bank and the Netherlands Authority for the Financial Markets. Rabobank London Branch is authorised by the Prudential Regulation Authority (“PRA”) and subject to regulation by the Financial Conduct Authority and limited regulation by the PRA. Details about the extent of our regulation by the PRA are available from us on request. Registered in England and Wales No. BR002630. An overview of all locations from where Rabobank issues research publications and the (other) relevant local regulators can be found here: https://www.rabobank.com/knowledge/raboresearch-locations

The information and opinions contained in this document are indicative and for discussion purposes only. No rights may be derived from any transactions described and/or commercial ideas contained in this document. This document is for information purposes only and is not, and should not be construed as, an offer, invitation or recommendation. This document shall not form the basis of, or cannot be relied upon in connection with, any contract or commitment by Rabobank to enter into any agreement or transaction. The contents of this publication are general in nature and do not take into account your personal objectives, financial situation or needs. The information in this document is not intended, and should not be understood, as an advice (including, without limitation, an advice within the meaning of article 1:1 and article 4:23 of the Dutch Financial Supervision Act). You should consider the appropriateness of the information and statements having regard to your specific circumstances and obtain financial, legal and/or tax advice as appropriate. This document is based on public information. The information and opinions contained in this document have been compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness.

The information and statements herein are made in good faith and are only valid as at the date of publication of this document or marketing communication. Any opinions, forecasts or estimates herein constitute a judgement of Rabobank as at the date of this document, and there can be no assurance that future results or events will be consistent with any such opinions, forecasts or estimates. All opinions expressed in this document are subject to change without notice. To the extent permitted by law Rabobank does not accept any liability whatsoever for any loss or damage howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of Rabobank. The distribution of this document may be restricted by law in certain jurisdictions and recipients of this document should inform themselves about, and observe any such restrictions.

A summary of the methodologies used by Rabobank can be found on our website.

Coöperatieve Rabobank U.A., Croeselaan 18, 3521 CB Utrecht, The Netherlands. All rights reserved.