The global poultry industry continues to operate with strong momentum. RaboResearch predicts robust poultry demand in 2025, with growth rates between 2.5% to 3%, following a 2.6% increase in 2024. Poultry remains an affordable protein option for price-conscious consumers due to its competitive pricing relative to other proteins.

Markets in South and Southeast Asia are expected to be the fastest growing in 2025, with countries like India, the Philippines, Vietnam, and Indonesia projected to see growth rates between 3% and 5%. The EU poultry market is also projected to accelerate its growth, with an expected increase of more than 3% this year.

In contrast, North and South America are facing supply challenges due to a global shortage of breeding stock and disappointing livability figures, particularly in North America. These issues are balancing markets but limiting the industry’s growth potential.

In our base case, we expect feed prices to remain flat. This is favorable for the industry relative to the past few years, which saw significantly higher feed prices in many parts of the world. The biggest operational concerns, aside from the potential impact of geopolitical disruptions, are the ongoing risks of highly pathogenic avian influenza (HPAI) and trade disruptions. Additionally, the supply of parent stock remains tight and hatching egg prices are still high, restricting growth. Rising egg prices are now driving renewed interest in vaccination as a tool to combat avian flu threats.

Global trade is expected to remain strong amid relatively tight global protein supply and growing consumption. However, growth will be in line with last year’s trend, remaining below the market growth rate of approximately 2% to 2.5% for 2025.

Geopolitics will be the most significant factor to watch in 2025. Rising geopolitical tension, including US tariffs on imports and retaliatory tariffs on US poultry from affected regions, could lead to a trade war and shifting global trade flows. Global traders should be prepared to respond quickly to developments in this area. Brazil and Thailand are expected to benefit from these geopolitical tensions. They are already gaining market share, and this trend is likely to continue. Indirectly, this could also lead to changes in operations due to restrictions or shifting trade flows of inputs like commodities and feed additives.

Global Poultry Markets Summary

US: Strong domestic market

- Limited production growth continues, as productivity challenges limit expansion

- Domestic demand strengthens due to robust foodservice sales in response to record beef prices

- Exports remain sluggish due to high prices, a strong USD, and rising geopolitical

Europe: Ongoing strong market context

- Chicken consumption shows ongoing strength (+3% to 4%).

- Chicken prices rise in Q1

- EU export volumes are increasing

- The relocation of production to southern and eastern European countries continues.

China: Oversupply challenges

- Increasing local production and stagnant demand continue to pressure prices, creating a context of ongoing oversupply challenges.

- Imports are likely to remain low in 1H due to price weakness and sufficient supply.

Brazil: Historically high exports

- Exports in January reached 430,000 metric tons, marking the best result for the month in history.

- Chicken gains a competitive edge compared to beef early in the year, positively impacting local prices.

Thailand: Peaking export volumes

- Export volumes, particularly processed chicken exports to Europe, reach historic highs.

- Rapid growth in domestic tourism supports a rebound in demand.

- Prices improve due to a more balanced domestic market

Japan: Rising chicken consumption

- Household chicken consumption remains strong, and foodservice demand recovers on the back of prolonged inflation and higher spending power.

- Chicken imports will rise slightly, as production remains flat

Global market outlook: Historically strong global production growth, concentrated in Asia, Europe and Africa

Profitability across regions

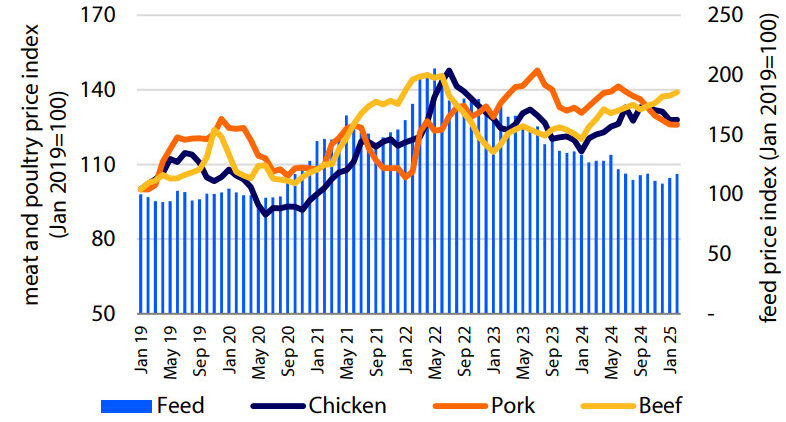

The global poultry industry’s strong momentum continues, with global consumption growth predicted to reach 2.5% to 3% this year. Improved economic conditions in many regions, together with ongoing high prices for other proteins, make poultry an attractive option for consumers worldwide and local demand robust (see figure 1).

This marks the second consecutive year of above-average market growth, which has led to significant improvements in margin performance in many regions. The improvement reflects lower feed costs and supply-demand balance due to tight breeding stock supply, avian flu outbreaks, and declining liveability figures in some regions, especially North America.

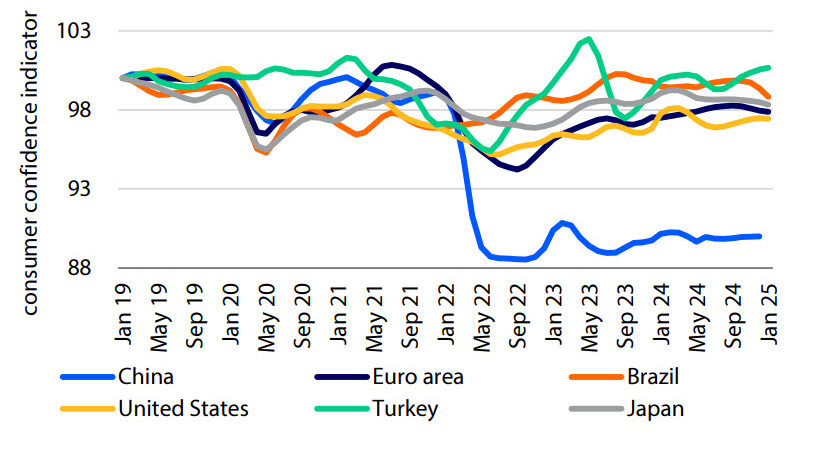

Almost all regions currently enjoy profitable market conditions, including the EU, UK, US, Brazil, Mexico, South Africa, Russia, Turkey, Thailand, Vietnam, and now also Japan. The notable exception is China, which faces an oversupplied domestic meat market after years of rapid expansion following the 2018 African swine fever outbreaks. Demand in China has slowed due to weaker economic conditions and waning consumer confidence (see figure 2). India and the Philippines have also experienced some setbacks in market conditions but are still operating around breakeven levels.

Ongoing above-average demand

The global poultry outlook for 2025 remains strong. Most market fundamentals still look robust, with ongoing strong demand for chicken, high beef prices, and projected flat feed prices. Chicken production is expected to remain steady in many markets, as avian flu and tight breeder availability are slowing restocking and production growth.

Global chicken supply is tight, as reflected in the high prices for hatching eggs in global markets, and avian flu continues to challenge production and trade.

Although these fundamentals look positive, it is crucial to keep supply growth in line with market growth. The Philippines and India are currently experiencing setbacks in their local markets after supply growth surpassed demand in recent months.

Global trade will remain strong, with Brazil and Thailand likely to be winners. They have already benefited from rising geopolitical tensions through increased market share in export markets like China and Mexico. This growth might continue in the coming years, especially if trade tensions escalate. Additionally, Brazil’s animal disease status is more favorable than that of the US and EU.

A peace agreement in Ukraine could significantly affect global and regional markets, as Ukraine is one of the most competitive suppliers of poultry and feed grains. If Ukraine gains more access to the EU market, it could shake up EU markets and substantially impact markets in the Middle East. This could challenge the position of local suppliers and exporters like Brazil and Thailand.

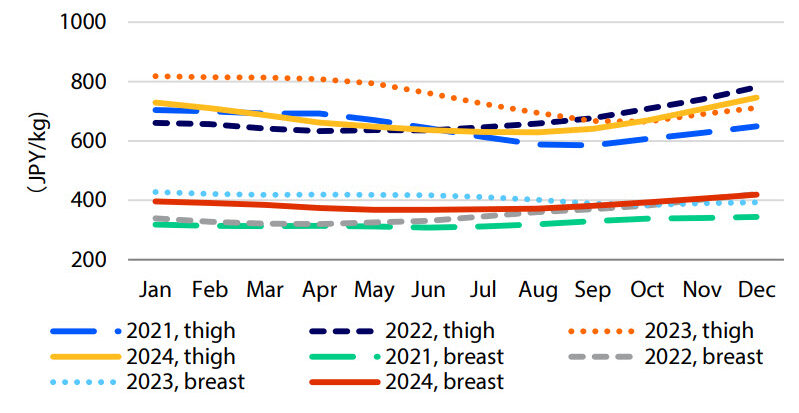

Figure 1: Global meat and feed price monitor, Jan 2019 – Feb 2025

Figure 2: OECD consumer confidence index, Jan 2019 – Jan 2025

Source: Bloomberg, IMF, Food & Agriculture Organization of the United States, OECD, RaboResearch 2025

Supply outlook: Heightened operational focus needed in times of geopolitical tensions and high avian flu pressure

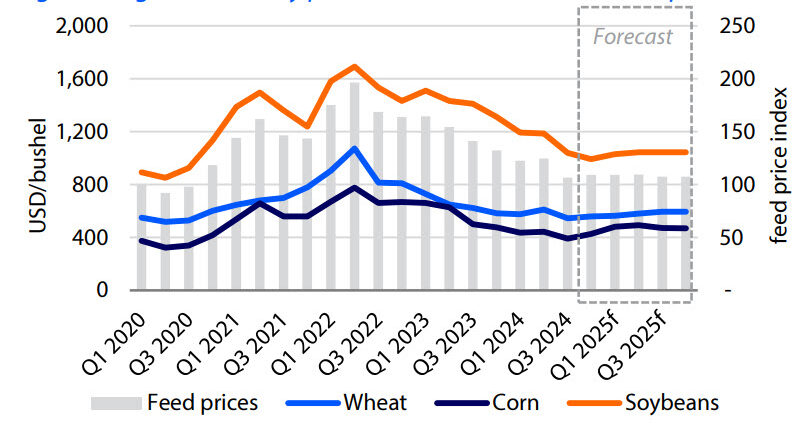

Feed price outlook: Flat base case, but weather and geopolitics pose risks

Agri commodity prices have been under pressure recently due to various factors, including US dollar weakness, geopolitical developments, such as a potential peace deal between Russia and Ukraine, and economic statecraft, particularly tariffs, affecting commodity markets. Additionally, weather conditions are playing a significant role in driving price volatility for most feed grains.

Wheat prices have risen due to cold temperatures in the US and Russia, which, coupled with deficient snow cover, pushed speculators to cover shorts and supported prices. Corn had a bullish start to 2025, with crop yield concerns in South America supporting higher prices. Late-crop corn is most at risk, and recent US spring planting acreage estimates are leading a sizable correction.

Soybean markets are experiencing lower prices due to the anticipated record crop in Brazil and uncertain import demand from China. Oversupply and weak fundamentals weigh on sentiment, although speculators moved back into a narrow long position at the start of 2025 due to corn price strength.

Our agri commodity price outlook base case indicates relatively flat feed prices for the remainder of 2025 but with rising uncertainties due to geopolitics and weather (see figure 3). Regions differ significantly, with recent price increases in South and Southeast Asia and Europe and more bearish conditions in southern Africa.

Avian influenza: Will US outbreaks drive change in production practices?

Dealing with avian influenza remains a significant challenge for the global poultry industry. The US has experienced the most substantial impact, with more than 36m birds culled this year, primarily in the layer sector. This has driven historically high egg prices and led to supply shortages in the US.

Introducing vaccination as a tool to reduce the risk of avian flu is now being discussed. The poultry industry has debated the use of vaccines in recent years. However, the US chicken industry has decided against adopting vaccines as a practice, due to mixed results in controlling the spread of disease and the potential for export disruptions.

Still, some countries have successfully introduced vaccines. For example, France suffered heavily from avian flu, especially in southwest regions of the country, which traditionally have high numbers of duck and Label Rouge (outdoor) production. Since adopting vaccination, France has seen significantly fewer cases, and domestic supply has fully recovered.

In other regions, avian flu remains a concern. Many of the HPAI outbreaks in Europe have occurred in central Europe but have not had a significant negative impact on the industry this year. Turkey experienced outbreaks in Q4 2024, affecting its export position for poultry. Australia continues to struggle with avian flu cases, impacting the local egg market. India, the Philippines, Taiwan, South Korea, and Japan are also reporting outbreaks but not at the same level as the US this year.

Figure 3: Agri commodity price outlook forecasts flat feed prices

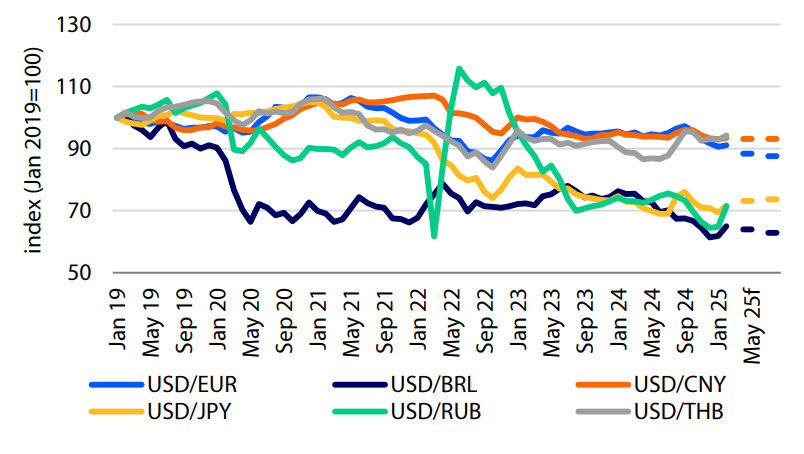

Figure 4: FX developments – strong USD, weaker EUR and BRL

Source: Bloomberg, national statistics bureaus, CBOT, MATIF, RaboResearch 2025

Global Poultry Trade: Ongoing strong conditions in global trade, geopolitics could shake up global trade flows

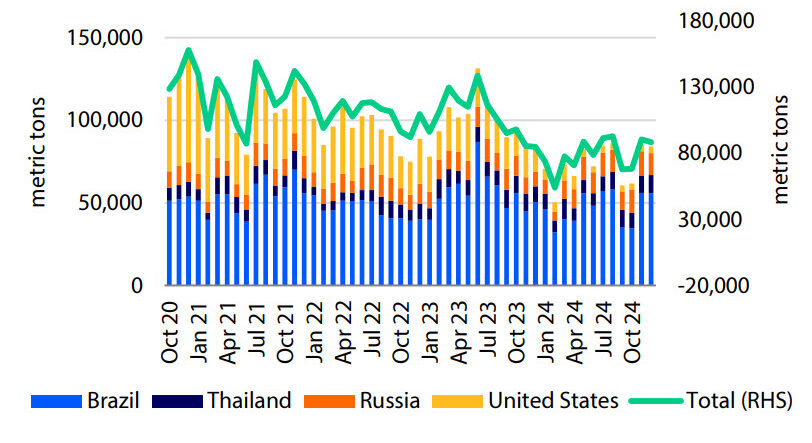

Global chicken trade: New records in Q4 2024, trade flows shift

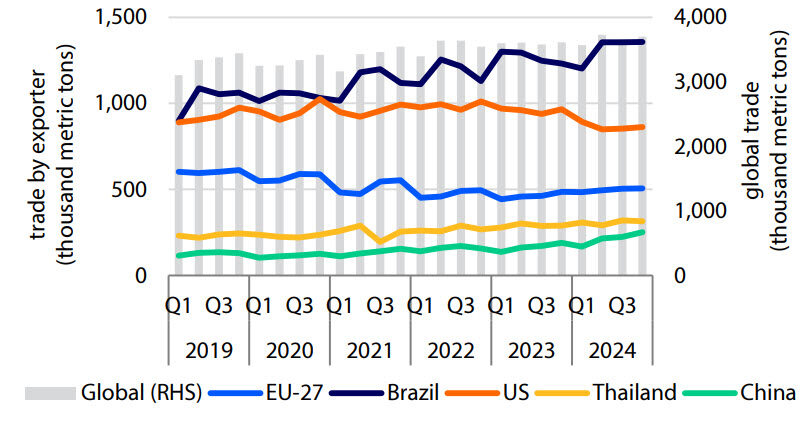

Global chicken trade reached a record 4.7m metric tons in Q4 2024, which is 3.5% (or 200,000 metric tons) more than Q4 2023 (see figure 5). Trade to the UK, the EU, Japan, Taiwan, Colombia, and the Middle East was strong, while Chinese imports continued to fall due to weak local market conditions.

Brazil emerged as the winner, capturing growth of 200,000 metric tons YOY in Q4 2024. The US lost 100,000 metric tons, primarily due to higher local prices (also for dark meat) and a significant drop in exports to China. EU exports grew slightly, while Thailand and China both continued to increase their exports. Turkey saw an ongoing drop in exports due to restrictions aimed at rebalancing local markets after avian flu outbreaks. Ukraine and Russia continued to grow their exports, with Russia now the second-largest exporter of chicken to China, surpassing the US and Thailand. Ukraine expanded its export position to the Middle East, benefiting from Turkey’s reduced exports.

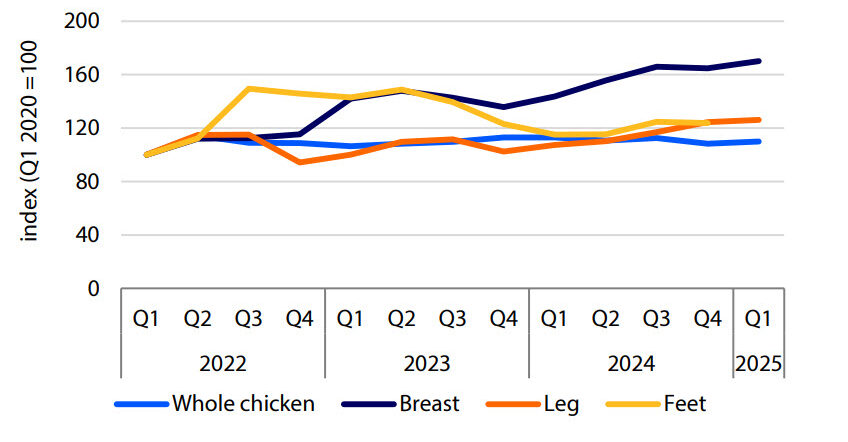

Global chicken prices have been steadily rising from their Q4 2023 lows. Prices in Q4 2024 were 5% higher than the previous year, with breast meat prices particularly strong (see figure 6). These high prices reflect tight global supply, especially in key import markets.

Processed chicken trade: Booming exports, especially to Europe

Global processed chicken trade reached a record 400,000 metric tons in Q4 2024, which is 15% above Q4 2023. Thailand benefited the most, increasing its exports by 30,000 metric tons to 180,000. China also saw an increase, with trade rising by 10,000 metric tons to 90,000. This growth is a notable achievement for the Thai industry, especially considering that the pricing position of Thai products compared to Chinese processed chicken products worsened in 2024 and early 2025. Thai processed chicken exports were, on average, 35% more expensive than Chinese products, up from 25% in Q4 2023. Trade has been especially strong to the UK, the EU, and, to a lesser extent, Japan.

Meanwhile, the EU’s processed meat exports remained flat at 45,000 metric tons in Q4 2024.

Global trade outlook: Strong prospects, but geopolitics could disrupt flows

Global poultry trade is expected to stay strong throughout the year. Although Q1 is typically a slow season, it is expected to surpass year-on-year levels due to ongoing tight market conditions in key import markets such as the EU, UK, and Middle East, as well as improved market conditions in Japan and Southeast Asia. Strong import demand is expected to persist throughout the year, keeping breast meat prices high. However, weak Chinese demand and local oversupply may limit upside.

Aside from the ongoing avian flu risks, rising geopolitical tensions and competition pose the biggest challenges for global trade. Recent import levies imposed by the US on China have already led to retaliatory levies by China on US chicken trade. Additionally, the EU has introduced anti-dumping levies on lysine imports from China, which is already affecting the EU lysine market in terms of prices and availability.

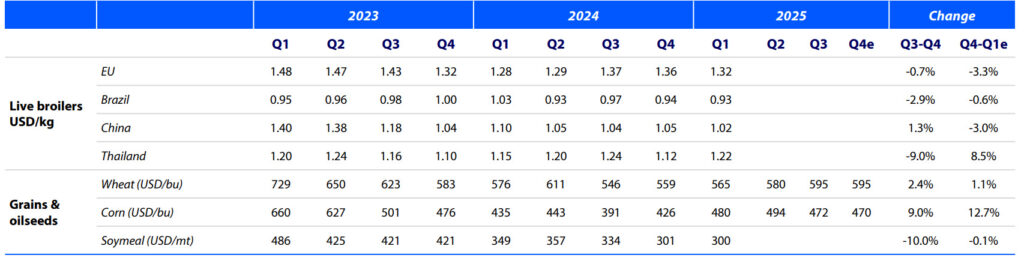

Figure 7: Live chicken, grain and oilseed price monitor

Figure 5: Global poultry trade: Strong Brazilian and Chinese exports

Figure 6: Chicken trade prices: Robust breast meat prices

Source: Bloomberg, national statistics bureau, RaboResearch 2025

Live chicken and chicken cut price monitor

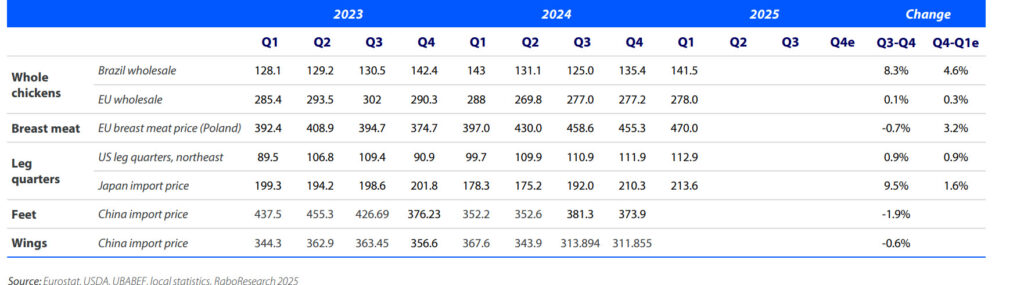

Figure 8: Chicken cut price monitor

US—Margin strength is a powerful growth incentive, but obstacles remain

US production gradually increasing, despite productivity challenges

Ready-to-cook chicken production is averaging 2.2% above year-ago levels, as heavier-weight birds (+2.1% YOY) more than offset the negligible increase in chicken availability. While the industry continues to set additional eggs to increase bird supplies, hatchability remains near historic lows at 78.9%. Low hatch rates, combined with ongoing livability issues, continue to limit expansion in slaughter. Integrators remain profitable at current production levels, given strong prices and ongoing moderation in feed costs due to ample domestic soymeal supplies. Based on projected profitability and production trends, RaboResearch forecasts a 1.6% YOY increase in chicken production in 2025.

Domestic demand strong, as chicken remains a good value

Chicken prices continue to average ahead of year-ago levels, due to stronger seasonal demand, increased foodservice interest, and rising retail promotional activity. Improved foodservice support for breast meat and tenders has strengthened prices compared to last year, with increases of 32% and 12%, respectively. Strong dark meat prices are also boosting composite values, driven by domestic demand for boneless thigh meat. Looking ahead, we expect record beef prices to continue supporting chicken demand in foodservice and retail channels. Historically low inventories of chicken in cold storage, down 3.1% YOY to 803m pounds, are also supportive, despite a modest increase in breast meat inventories during the month. We remain optimistic about the price outlook for 1H 2025, given our current demand outlook and expectations for relatively steady production growth despite incentives for increasing supply growth.

2024 ended with weaker exports, stabilization unlikely in 2025

US chicken export volumes at the end of the year were weak, down 17.7% YOY to 255,470 metric tons, while total export value fell by 1.3% YOY. Weaker sales to Mexico (-4.2% YOY), Cuba (-29% YOY), and China (-24% YOY) drove the decline and more than offset stronger shipments to Guatemala, Canada, and Vietnam. For the full year 2024, US chicken exports were down 10% YOY in terms of volume, but the total export value remained flat at USD 4.7bn, the same as the previous year. HPAI-related disruptions and rising geopolitical tensions limited trade during the year, as did relatively high leg quarter prices (+16% YOY) through Q4 2024. Exports were weak to start of the year, down 20.5% in January in volume and 5% in value. Among the top markets, only exports to Mexico, Canada, and the Dominican Republic were higher compared to the same month last year. Exports are expected to remain below five-year averages due to continued trade disruptions, particularly given the risk of retaliatory tariffs from partners like Canada, China, and Mexico.

Figure 9: Breast meat prices steady and well ahead of year-ago levels

Figure 10: Chicken exports show limited growth through September

Source: USDA, RaboResearch 2025

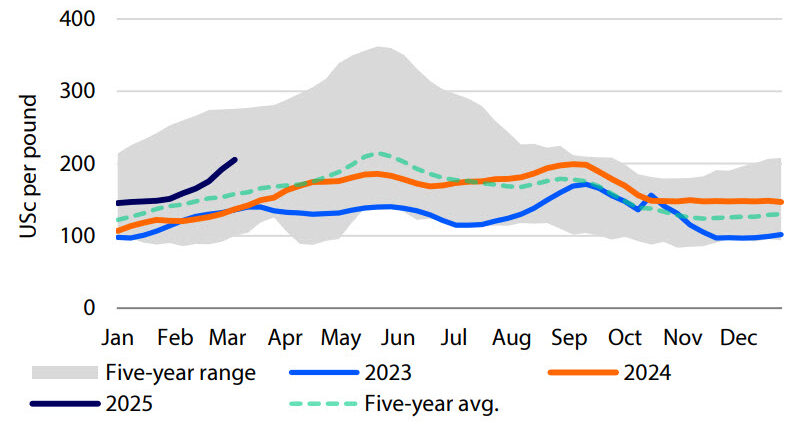

Mexico—Live chicken and parts pricing moves sharply upward on limited supplies

Live chicken prices up due to limited availability

Live chicken prices increased at the start of 2025. Currently, prices are at MXN 36.73/kg, which is 17.8% above the five-year average and 32.2% higher than the price on December 1, 2024 (see figure 11). This price increase is due to livability issues on the production side. To address this, producers have been bringing product to market sooner, resulting in a stabilization of prices through January 2025. Once this initial supply is worked through, we can expect additional support for prices. This trend should continue into Q2, as production needs to stabilize to achieve any significant downward shift in prices.

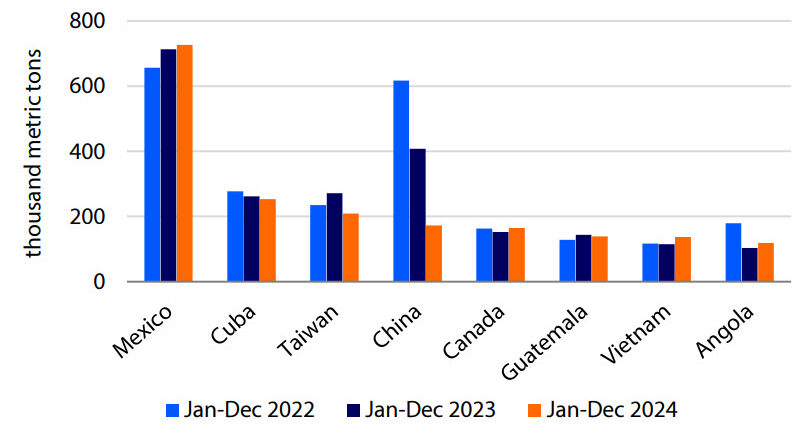

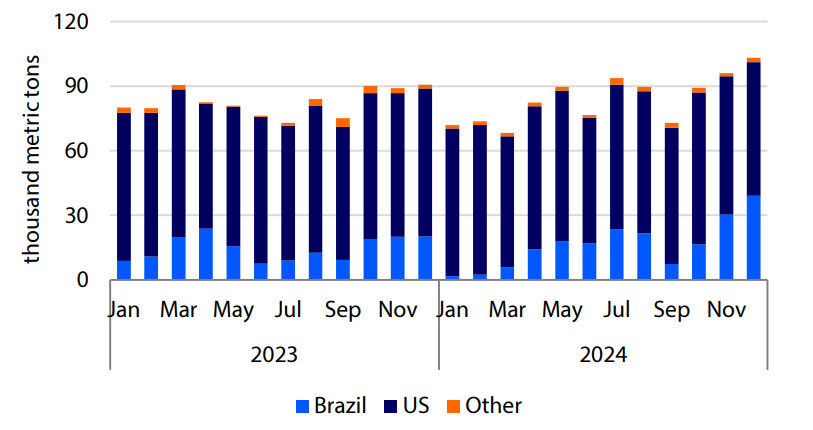

Brazil continues to gain share of Mexican chicken imports

Mexico’s chicken imports ended 2024 up just 1.6% YOY for a total of 1m metric tons. Among countries exporting to Mexico, Brazil was the only supplier with a significant increase in shipments, rising 12.0% YOY. The US maintained its year-ago shipment levels, down just 0.6%. However, compared with Q3 shipments, Mexican chicken import volumes increased by 6.9% compared to the same period in 2023, with over 100,000 metric tons being imported in December alone. Due to current political tensions between the US and Mexico, more product is being sourced from Brazil now. In November and December 2024, Brazil accounted for 32% and 38% of imports, respectively (see figure 12). These were both new highs for the past two years. Until trade negotiations with the US are completed, and depending on the outcome, expect more imports from Brazil.

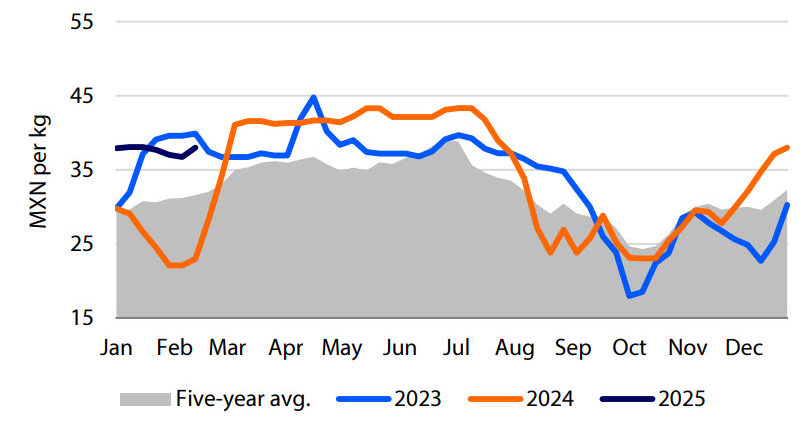

Chicken prices receive support as consumers trade down

Parts pricing has received the same price boost as live birds. The whole chicken price is now MXN 69.59/kg, up 69.6 % YOY. The breast price is MXN 120.50/kg, a 43.8% YOY increase, and the thigh price is MXN 58.50/kg, 31.1% above a year ago. These price increases are due to the relatively tight supply and the trade-down effect, with consumers opting for cheaper alternatives due to the higher prices of other proteins, generating solid demand. Beef cutout prices are at record highs, and pork prices are near record highs, causing consumers to search for lower-cost alternatives. This has supported chicken prices, particularly for whole birds, as they are generally one of the cheapest protein options in Mexico. Mexico’s economy is highly dependent on the US. Changing administrations in both countries, followed by trade negotiations, have lowered economic growth indicators for 2025. This will continue to weigh on consumer optimism, further driving consumers to trade down to lower-cost options. As a result, chicken prices should remain supported until there is some level of certainty around trade.

Figure 11: Live chicken prices could receive additional support

Figure 12: Brazil’s share of Mexican chicken imports hits record high

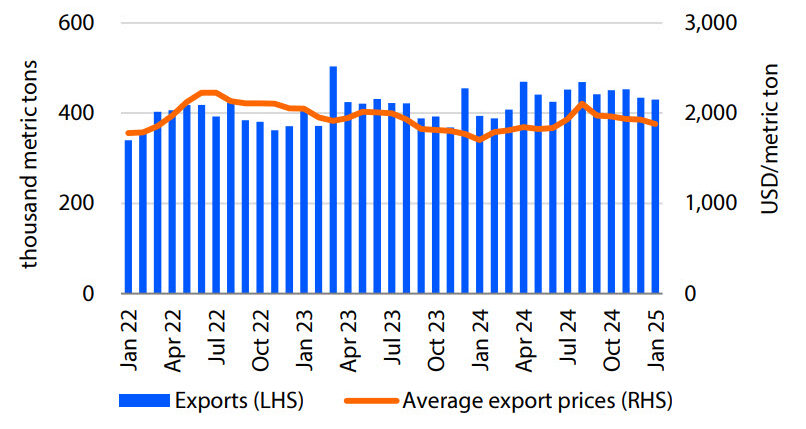

Brazil—Heated domestic and external demand boosts live broiler and chicken prices

After a record year in 2024, chicken exports start 2025 strong

Brazilian chicken exports set a record for the fifth consecutive year in 2024, reaching 5.2m metric tons and generating USD 9.9bn in revenue, reflecting increases of 4% and 3% YOY, respectively. The start of 2025 has also been promising, with January’s shipments totaling 430,000 metric tons, a 9% YOY increase and the highest volume ever recorded for the month. Revenue for January was USD 809m, marking robust 21% YOY growth, second only to January 2023’s USD 838m. Preliminary data up to the third week of February indicates a significant 22% YOY increase in daily shipments.

China remains the primary destination of Brazilian chicken exports, accounting for 10% of Brazil’s total chicken shipments and showing a 15% YTD increase. The UAE follows with a slight 0.5% YTD rise, while Saudi Arabia and Japan experienced declines of 9% and 30%, respectively, over the same period. Notably, the Philippines saw a 39% YTD increase, and Mexico recorded a substantial 651% rise, from 1,000 metric tons to approximately 11,000, following the renewal of the Mexican government’s food security program, which directly benefited Brazilian exports. The onset of colder seasons in the Northern Hemisphere, leading to a rise in HPAI cases, coupled with reduced shipments from key markets like the US, has driven increased demand for Brazilian chicken, which remains resilient despite rising feed costs, particularly for corn.

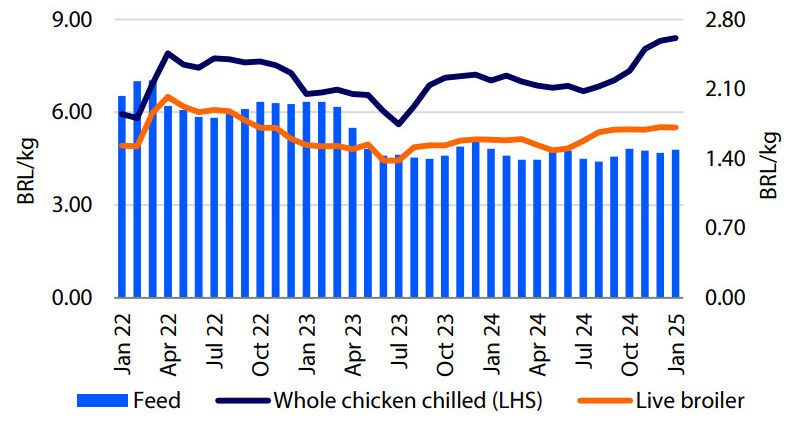

Brazilian chicken production also reached a record high

Preliminary data on chicken meat production in Q4 2024 indicates a 5% YOY increase, resulting in a record supply of 13.6m metric tons, a 2.3% rise compared to the previous year. In addition to robust external demand, the significant increase in beef prices during 2H 2024 directly enhanced the competitiveness of chicken meat at the beginning of this year, prompting a portion of the population to shift to more affordable proteins. The sharp rise in egg prices at the start of the year, driven by a severe heat wave in key producing regions and the increase in corn prices, has also contributed to this increased demand for chicken, as the price difference between eggs and chicken has declined. This trend is expected to remain strong at least until the end of Lent in mid-April.

Figure 13: Shipments continued at a record pace in Jan 2025

Figure 14: Heated demand supports appreciation of chicken prices

Source: Secex, Cepea, IBGE, RaboResearch 2025

Europe—Ongoing positive outlook for European Poultry Products

Ongoing strong market conditions for the European poultry industry

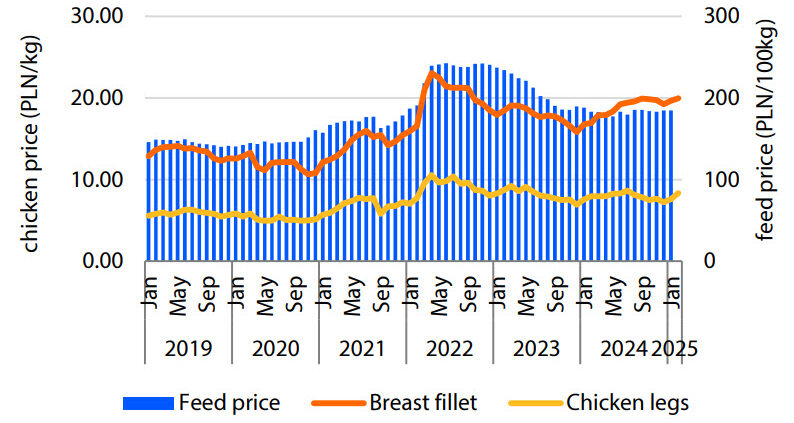

The European poultry industry is maintaining its strong momentum, with chicken prices steadily increasing (see figure 15). In Q1 2025, EU broiler prices have risen 15% YOY, following a dip November. Ongoing strong demand, coupled with tight supply, is keeping prices high across Europe.

Total European chicken consumption in 2024 increased 5%, achieving record growth. Chicken’s strong price position compared to other proteins like beef and pork has significantly benefited the market, especially during times of economic uncertainty and heightened price consciousness among consumers. Additionally, increasing implementation of sustainability strategies supports retail and foodservice demand for chicken versus other animal proteins.

Prices for breast meat are currently moving above their previous record high of 2022. Prices for leg meat and wings are also improving after a period of weakness in 2H 2024.

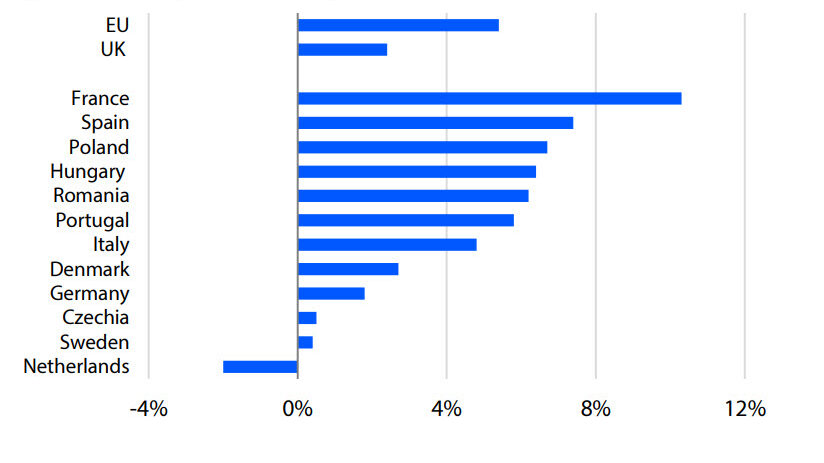

Production growth at historic highs

Strong domestic demand for chicken in the EU has given the industry room to grow. Total production in the EU increased more than 5% YOY in 2024, while UK production growth was slower at 2.4%. Ongoing implementation of animal welfare-related farming concepts in northwest Europe has led to lower production growth in those markets (see figure 16). Most UK retailers are currently transitioning to 20% lower density at broiler farms, which will affect supply in 2025. The rapid growth of chicken production in France is partly due to recovery following avian flu outbreaks and the success of its vaccination program. Growth in Spain, Hungary, Poland, and Romania is in line with expectations, with an ongoing shift in production from northwest Europe to the east and south of Europe.

Despite high domestic prices in Europe, exports have been developing well, with export volumes growing 9% in 2024, driven by strong demand from Vietnam, DRC, Uzbekistan, and the reopening of the Philippines after HPAI-related export restrictions were lifted. Exports to the UK have increased by 4%, mainly due to more Polish exports, on the back of tight domestic supply in the UK.

Chicken imports in the EU were slightly down (2%), mainly due to a drop in imports from Brazil (-6%) and Ukraine (-19%) – the latter due to the country’s self-imposed export restrictions.

Positive outlook with challenges from pork prices and Ukraine access

The outlook for the EU poultry industry remains strong, with volume expected to grow 3% to 4% this year. Market conditions are expected to remain favorable. However, uncertainties could impact the outlook. Although beef prices remain high, the decline in pork prices could alter the competitive position of chicken in the market. Moreover, the expiration of Ukraine’s voluntary export restriction in May 2025 is another wild card. If Ukraine resumes selling unlimited volumes of chicken, it could negatively affect the market in 2025, similar to the impact seen in 2022/2023.

Figure 15: Chicken and feed prices in Poland, Jan 2019 – Jan 2025

Figure 16: European chicken production, 2024 vs. 2023

Source: Eurostat, RaboResearch 2025

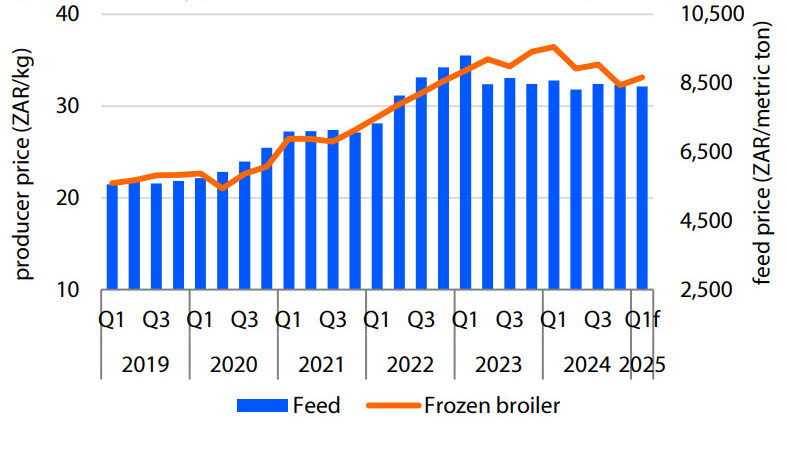

South Africa—Outlook for 2025 is positive with rising demand and lower costs

Lower chicken prices year-on-year, peaking consumption

Market conditions in South Africa have been improving in Q1 2025, with chicken prices 3% higher and feed costs slightly lower (-1%) compared to Q4 2024. Although prices are currently slightly above the previous quarter, they are 9% lower compared to Q1 2024 levels. Lower prices throughout 2024 and 2025 have made chicken more affordable (see figure 17). This greatly supported demand in South Africa, which saw total chicken consumption increase 12% YOY in Q4 2024.

The market in South Africa is highly price-driven due to the relatively high share of consumers in low- income groups. Consumer price inflation over the last few years, combined with high energy prices, has significantly impacted these consumers. The drop in chicken prices has made chicken more affordable for this segment, leading to strong demand for individually quick-frozen chicken packages.

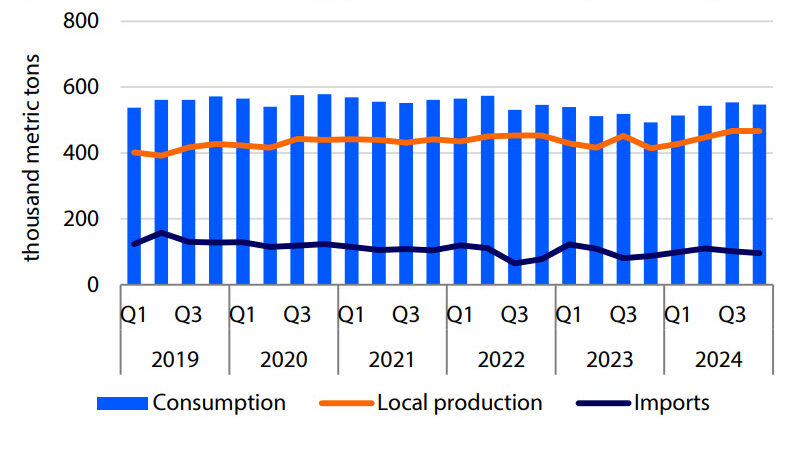

Rising production and imports

Lower prices and strong demand are significantly supporting the South African chicken industry. Profitability has been improving, allowing the industry to expand production again. Total chicken production in South Africa increased 13% YOY in Q4 2024. It’s important to note that Q4 2023 was heavily impacted by avian flu, resulting in very tight supply and high prices in Q4 2023 and Q1 2024. The industry recovered quickly by importing hatching eggs but still fears outbreaks of new cases and is lobbying for the acceptance of vaccination as a tool to deal with the increased risk of avian flu as winter approaches.

Imports also grew, rising 10% YOY, mainly due to a rapid increase in mechanically deboned meat imports (+30%) and, to a lesser extent, chicken feet (+2%).

Positive outlook amid lower costs

The outlook for the South African industry is positive. The industry is anticipating a significantly improved crop harvest this year after a major El Niño event impacted the 2023/24 crop year, leading to reduced production and high feed prices. Currently, weather conditions are favorable, and the industry expects much better yields than last year. Summer crop production is projected to increase 30% YOY to 17m metric tons, sunflower is expected to rise by 14% YOY, and soybean production is forecast to grow by 40%. SAFEX indicates a 15% drop in corn prices during the year, while soybean prices are expected to decrease by 5% in South Africa.

Lower feed costs will help make chicken even more affordable and could further stimulate chicken consumption. Additionally, “loadshedding” costs incurred due to planned power outages have been decreasing this year, further reducing industry expenses. However, water availability remains a significant concern for producers.

Given this favorable context, the South African poultry industry has opportunity to grow production by around 2% to 3% this year. Avian flu remains a wild card. Risks persist, and the winter season will soon arrive with its typically higher risk of outbreaks. Currently, the government’s voluntary vaccination program mitigates these risks.

Figure 17: Poultry prices bounce back after a weak Q4

Figure 18: South African supply sees more local output, less imports

Source: SAPA, News24, SAFEX, RaboResearch 2025

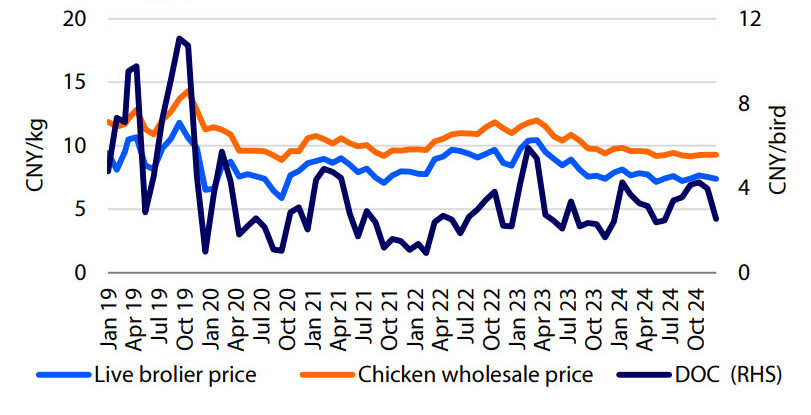

China—Poultry prices remain pressured due to oversupply

Poultry prices remain weak

Poultry prices remained pressured in the first two months of 2025. In February, live bird prices fell below CNY 7/kg, down 10% MOM and 20% YOY. Slow market sales following the Chinese Lunar New Year and rising domestic production were the main drivers behind the price volatility. Day-old chick (DOC) prices saw a steeper decline, from over CNY 4 per bird in December 2024 to below CNY 2 in February (see figure 19). Based on official data, China’s poultry production rose by 3.8% YOY in 2024, reaching 26.6m metric tons. Poultry’s share of China’s total meat production increased from 23% in 2018 to 27% in 2024, due to poultry production’s faster growth compared to other proteins. We expect poultry production to continue growing in 2025 but at a slower pace than in 2024, as major players continued to invest in new production facilities in 2024 despite the price weakness. This will exert additional pressure on market prices in 2025. In addition to overcapacity challenges, a reduction in production costs following a 10% YOY decline in feed costs in 2024 contributed to lower prices. We expect production costs to trend down further in 2025, but with some volatility, as soymeal prices fluctuated in the first two months of the year, affecting producers’ feed procurement strategies. In an oversupplied market, we foresee intensifying competition and further consolidation in the year ahead.

China has suspended imports of grandparent stock (GPS) from the US and New Zealand. According to a China Customs announcement, China has resumed imports of GPS from Spain, but these have not arrived in the market yet. Until these imports begin, GPS supply will rely on local production in the near term, providing growth opportunities for local breeding companies.

Poultry imports expected to stay low in 1H 2025

Chinese poultry imports declined significantly in 2024, down 25% YOY, to 971,000 metric tons. Brazil, the largest exporter, saw an 18% YOY decrease in exports to China, while Russia and Thailand, the second and third largest suppliers, showed either small growth or a marginal decline.

Conversely, Chinese poultry exports increased significantly in 2024, up 39% YOY, taking advantage of strong demand in importing countries. As a result, the net trade deficit narrowed to 270,000 metric tons in 2024, down from 330,000 in the previous year. We expect poultry imports to stay low in 1H 2025, due to low prices and sufficient supply in the local market.

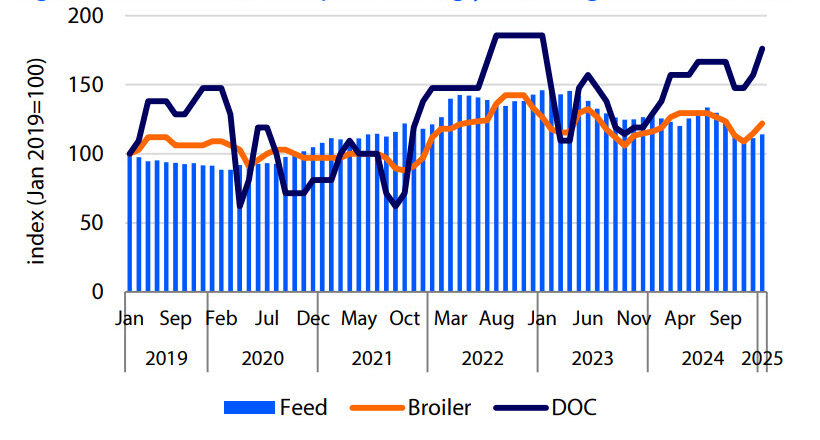

Figure 19: White feathered broiler prices remain pressured due to sufficient supply

Figure 20: Imports expected to stay low in 1H 2025

Source: MARA, China Customs, Boyar, RaboResearch 2025

Japan—Stronger demand for chicken, with a higher share of cheaper imported chicken

Imported chicken, which is cheaper relative to domestic, sees high demand

Consumers’ buying power remains weak because wage growth has not kept pace with persistent inflation, resulting in a shift in demand from beef and pork to chicken. In Q4, household chicken consumption per capita increased by 1.9% YOY, while beef and pork decreased by 1.7% and 1.3%, respectively. Looking at estimated market supply in Q4 (including household and foodservice consumption), domestic chicken consumption rose by 1.3% YOY, while imported chicken jumped 7.1% YOY. This indicates that the consumption of imported chicken, which is cheaper than domestic chicken, is growing amid rising labor and ingredient costs.

Demand for “jidori” (premium chicken) is weak, and the industry is planning promotions targeted at foreign visitors. With temperatures from March to April forecast to be warmer, demand for out-of- home consumption will be good. Consumption by foreign tourists is also expected to remain bullish.

Production to remain flat due to labor shortages

Japanese chicken production climbed 1.6% YOY in 2024, reaching a record high. However, a decline in production during the hot summer resulted in lower frozen stocks, which are usually sold at the end of the year when demand is highest. As Q4 2024 production was flat (-0.3% YOY) and supply was insufficient, wholesale prices were high from fall onward.

From October 2024 to January 2025, 660,000 broilers were depopulated due to HPAI outbreaks, which is equivalent to 67% of the record-high depopulation numbers in the 2022/23 season. Although production is almost going well, some farms have reported E. coli infections and poor weight gain, indicating that the supply-demand balance is expected to be a little tight during Q1.

Production in 2025 is expected to remain nearly flat year-on-year due to stagnating processing capacity, labor shortages, and the possibility of slowed production in the event of hot weather.

Import volumes to rise slightly year-on-year

Despite the weaker yen, Japanese import volumes of raw chicken and prepared chicken grew by 9.3% and 5.3% YOY respectively in 2024, due to increased demand from the foodservice and food-

processing industries. Import volumes of raw chicken and prepared chicken are expected to increase slightly in Q2 2025, compared to the previous year. This rise is driven by growing consumer demand for prepared food and the low-cost strategies of the foodservice and prepared food industries.

Figure 21: Wholesale chicken thigh and breast prices nearly reached 2022 levels in Dec 2024

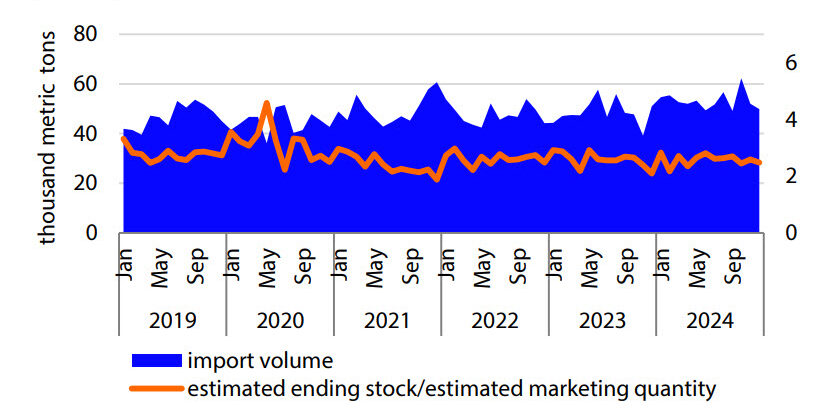

Figure 22: The ratio of imported raw chicken stocks to the marketing quantity has been stable

Source: ALIC, RaboResearch 2025

Thailand—Market conditions have turned positive in Q1, and the industry outlook is optimistic

Domestic market conditions significantly improved

The Thai poultry industry is experiencing better market conditions in Q1 2025. After an 8% drop in Q4 2024, prices have rebounded by 9% so far in Q1 2025. Stronger demand in both domestic and international markets, combined with tight DOC supply, has led to an improved performance in the industry. The tight domestic DOC supply has caused DOC prices to surge to near-record highs (see figure 23).

Domestic animal protein markets are currently improving. Meat consumption in Thailand has finally surpassed pre-Covid and pre-ASF levels, thanks to ongoing growth in tourism and strong economic growth. The prices of competing proteins like pork, eggs, and shrimp have reached their highest levels in two years, making chicken an affordable option for consumers (see figure 23).

Strong processed poultry exports drive Thai export growth

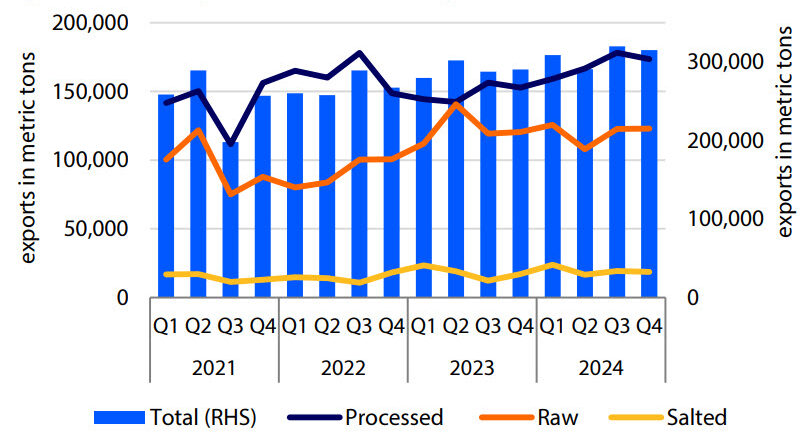

In 2024, Thailand’s total poultry exports grew 2%, to 1.2m metric tons. Processed poultry exports increased 14%, to 680,000 metric tons, while raw poultry exports grew only 3% to 480,000 metric tons (see figure 24). Additionally, salted breast meat exports increased a sizable 25%, driven by strong European demand.

In Q4, Thai poultry exports were even more bullish, with 9% YOY growth. Processed poultry exports grew by 14%, raw poultry by 2%, and salted breast meat by 9%.

The strong processed poultry export figures were mainly driven by demand from the EU and UK. Exports to Japan are also gradually recovering, with 6% YOY growth in Q4 due to tight local supply. Canada and UAE are emerging as export destinations for processed poultry. The weaker exports of raw chicken were primarily due to reduced shipments to China, South Korea, and Japan, while other export markets, such as Europe and Southeast Asia, continued to grow.

Outlook: Ongoing growth in production and exports

The 2025 outlook for the Thai poultry industry remains strong. Gradual improvements in global economic conditions, coupled with sustained demand for chicken in Europe and recovering market conditions in Japan, provide a solid base for ongoing growth in Thai poultry exports (approximately 2% to 3%). Domestic market conditions are also strengthening due to better economic conditions and increased tourism (Thailand aims for more than 30% growth in tourism numbers in 2025). Therefore, we expect Thai production to grow in 2025.

However, rising corn costs in Thailand are a concern. Prices have increased by 15% YOY due to tight local corn supply and higher international prices. The industry has been lobbying for a temporary easing of import conditions. On a positive note, soybean prices in Thailand have dropped.

Figure 23: Broiler and DOC prices strongly bouncing back in Q1 2025

Figure 24: Thai exports are at record-high levels

Source: Bloomberg, Thai Feed Mill Association, RaboResearch 2025

Report Authors

Lead author:

Nan-Dirk Mulder, nan-dirk.mulder@rabobank.com

Contributing authors:

Chenjun Pan – China chenjun.pan@rabobank.com

Christine McCracken – North America christine.mccracken@rabobank.com

Wagner Yanaguizawa – Brazil wagner.yanaguizawa@rabobank.com

Yuriko Katada – Japan katada_yuriko@nochuri.co.jp

Ms. Katada is an Analyst at the Norinchukin Research Institute, a part of Norinchukin Bank, Japan. She and Mr Hideki Obata have contributed to this quarterly under the terms of the partnership agreement between Rabobank and Norinchukin Bank

Disclaimer

This document is meant exclusively for you and does not carry any right of publication or disclosure other than to Coöperatieve Rabobank U.A. (“Rabobank”), registered in Amsterdam. Neither this document nor any of its contents may be distributed, reproduced, or used for any other purpose without the prior written consent of Rabobank. The information in this document reflects prevailing market conditions and our judgement as of this date, all of which may be subject to change. This document is based on public information. The information and opinions contained in this document have been compiled or derived from sources believed to be reliable; however, Rabobank does not guarantee the correctness or completeness of this document, and does not accept any liability in this respect. The information and opinions contained in this document are indicative and for discussion purposes only. No rights may be derived from any potential offers, transactions, commercial ideas, et cetera contained in this document. This document does not constitute an offer, invitation, or recommendation. This document shall not form the basis of, or cannot be relied upon in connection with, any contract or commitment whatsoever. The information in this document is not intended, and may not be understood, as an advice (including, without limitation, an advice within the meaning of article 1:1 and article 4:23 of the Dutch Financial Supervision Act). This document is governed by Dutch law. The competent court in Amsterdam, the Netherlands has exclusive jurisdiction to settle any dispute which may arise out of, or in connection with, this document and/or any discussions or negotiations based on it. This report has been published in line with Rabobank’s long-term commitment to international food and agribusiness. It is one of a series of publications undertaken by the global department of RaboResearch Food & Agribusiness. ©2025–All Rights Reserved