Summary

- We have updated our baseline forecasts to reflect the recent de-escalation in the tariff war between the US and China. We now expect a shallow recession starting in Q3 and the Fed to cut in September.

- However, the risks to our baseline are large, given the unpredictability of the trade war.

- In addition, there are risks from fiscal policy and monetary policy. The possible failure of the “one big beautiful bill” could cause a fiscal cliff at the end of the year that would have a negative impact on economic growth and inflation. In contrast, the conceivable loss of Fed independence would have an upward impact on growth and inflation.

Introduction

Last month, after running a range of trade war scenarios in a global macroeconometric model, we concluded that the probability of a recession in the US was larger than 50% (for details about the scenarios and the simulation outcomes, see A Tariff-Induced Recession?). In each scenario, the US economy contracted in Q3. Therefore, our recession forecast seems robust to a wide range of scenarios. The same is true for the rebound in inflation and the rise in unemployment. However, the depth and length of the recession depends on which scenario materializes.

Trade war de-escalation?

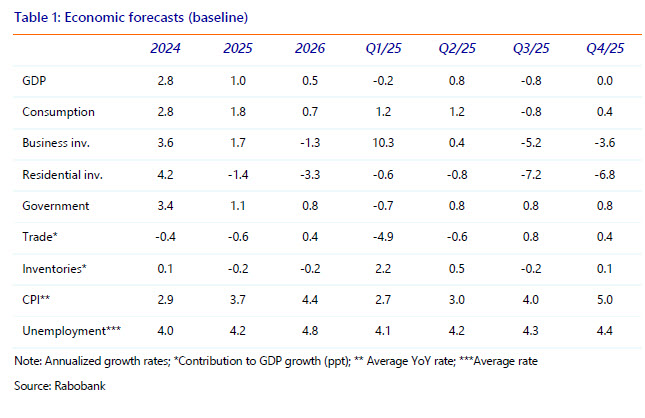

Trade negotiations are still in a state of flux, but there has been some notable de-escalation in tensions between China and the US. On May 12, this led to a 90-day delay in bilateral tariff hikes, reducing the additional US tariffs on Chinese imports from 125% to 10%. While our baseline economic forecasts were based on what we called scenario 1+ and 2+, with the plus indicating an escalation between the US and China, it now seems more likely that scenario 1 (“Negotiation”) and 2 (“Implementation”) will unfold, again with different outcomes for different countries. Our new baseline forecasts, which also incorporate more recent data and insights, are shown in table 1.

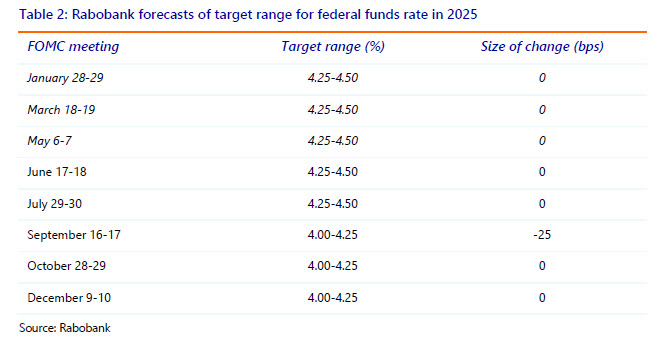

We still expect a recession, but a more shallow and shorter one than in last month’s forecasts. We think it will be shorter, because of a later start and an earlier end. This also means that we have become more optimistic about near-term data, which is also supported by the most recent data, and therefore we have also adjusted our Fed policy rate forecasts. In particular, we have moved our forecast of a rate cut of 25 bps from June to September. However, we still expect only a single rate cut, assuming that the FOMC will be torn between the two legs of its dual mandate once employment growth slows down and inflation rebounds. In contrast, markets are currently pricing in two rate cuts in 2025. Of course, trade negotiations could still re-escalate or they could lead to mutually beneficial outcomes. Next month we could have a different trade war scenario as our baseline. However, as we stressed in A Tariff-Induced Recession? all scenarios we considered led to negative GDP growth in Q3, a rebound in inflation and a rise in unemployment. So that forecast seems robust to a range of trade war outcomes. Therefore, we still think that the probability of a recession is higher than 50%.

One big beautiful bill or fiscal cliff?

While we looked at a range of trade war scenarios, to keep the analysis manageable, we kept our assumptions on fiscal and monetary policy constant. Starting with fiscal policy, the House of Representatives passed their version of what has become known as the “one big, beautiful bill” on May 22. Now it is up to the Senate to come up with their version. Once both chambers of parliament agree on the text, President Trump can sign it into law. The self-imposed deadline for the Republicans is Independence Day (July 4). Our forecasts – both the baseline and the alternative trade war scenarios – assume that a version of the One Big Beautiful Budget Act of 2025 will be adopted, in particular the extension of the income tax provisions in the Tax Cuts and Jobs Act of 2017. If the bill for some reason fails and we get a fiscal cliff at the end of the year, this would have a negative impact on our baseline forecasts for economic growth and inflation, and an upward impact on unemployment, especially in 2026.

Fed in wait-and-see mode

Turning to monetary policy, we assumed that the Fed can continue to pursue monetary policy independent from interference by President Trump. However, as we flagged a year ago in Trumping the Fed, and more recently in the International Banker magazine, we think that the Fed and Trump are on a collision course. If Trump manages to remove Powell prematurely and/or impose his will on the FOMC, we would surely see more rate cuts than we have assumed in our baseline scenario. This would have an upward impact on our forecasts for GDP growth and inflation and a negative impact on the unemployment rate.

However, for now we assume that Powell and the FOMC are free to pursue their dual mandate as they see fit. This means that they are facing a balancing act between maximum employment and stable prices. The upward impact of the tariffs on unemployment would ask for rate cuts to support economic activity. In contrast, the projected rebound in inflation could require rate hikes to slow down aggregate demand and get inflation under control. The stagflationary impact of tariffs pulls the Fed in two opposite directions. On balance, we think that the Fed will therefore be slow and modest in its reactions. For now, we expect only one rate cut in the second half of the year. The Fed has only limited room to come to the rescue of economic activity, because they also have to maintain their credibility as inflation fighters.

Conclusion

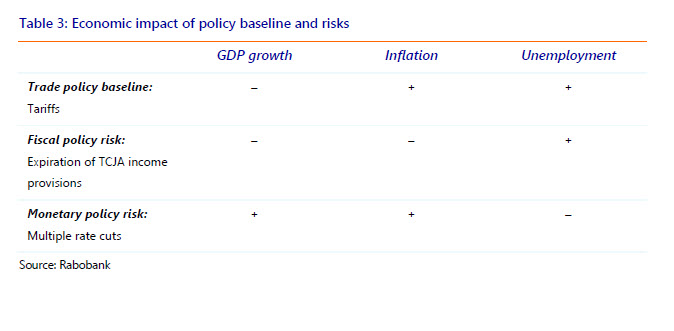

While we have updated our baseline forecasts to reflect the recent de-escalation in the tariff war between the US and China, it is important to realize that there are major risks to our new baseline. The trade war could re-escalate at any time or we may see some unexpected progress in the negotiations. At the same time, the Republicans are trying to pass one big beautiful bill through Congress with small majorities in both chambers of parliament. Meanwhile, the Fed is patiently waiting for these developments to provide some clarity about trade and fiscal policy. At the same time, President Trump is impatient about the rate cuts he wants to see from the Fed. We have summarized the economic impact of trade policy, fiscal policy and monetary policy in table 3.

Note that tariffs are our baseline, while an expiration of the TCJA income provisions and the loss

of Fed independence are risks that have opposite effects on the baseline outcomes. In these times of extreme policy uncertainty, understanding the economic impact of the key risks may be helpful.

Global Economics and Markets

Global Head

Jan Lambregts

+44 20 7664 9669

Jan.Lambregts@Rabobank.com

Macro Strategy

Global

Michael Every

Senior Macro Strategist

Michael.Every@Rabobank.com

Europe

Elwin de Groot

Head Macro Strategy Eurozone, ECB

+31 30 712 1322

Elwin.de.Groot@Rabobank.com

Bas van Geffen

Senior Macro Strategist ECB, Eurozone

+31 30 712 1046

Bas.van.Geffen@Rabobank.com

Stefan Koopman

Senior Macro Strategist UK, Eurozone

+31 30 712 1328

Stefan.Koopman@Rabobank.com

Maartje Wijffelaars

Senior Economist Italy, Spain, Eurozone

+31 88 721 8329

Maartje.Wijffelaars@Rabobank.nl

Americas

Philip Marey

Senior Macro Strategist

United States, Fed

+31 30 712 1437

Philip.Marey@Rabobank.com

Christian Lawrence

Head of Cross-Asset Strategy

Canada, Mexico

+1 212 808 6923

Christian.Lawrence@Rabobank.com

Mauricio Une

Senior Macro Strategist

Brazil, Chile, Peru

+55 11 5503 7347

Mauricio.Une@Rabobank.com

Renan Alves

Macro Strategist Brazil

+55 11 5503 7288

Renan.Alves@Rabobank.com

Molly Schwartz

Cross-Asset Strategist

+1 516 640 7372

Molly.Schwartz@Rabobank.com

Asia, Australia & New Zealand

Teeuwe Mevissen

Senior Macro Strategist China

+31 30 712 1509

Teeuwe.Mevissen@Rabobank.com

Benjamin Picton

Senior Macro Strategist Australia, New Zealand

+61 2 8115 3123

Benjamin.Picton@Rabobank.com

FX Strategy

Jane Foley

Head FX Strategy G10 FX

+44 20 7809 4776

Jane.Foley@Rabobank.com

Rates Strategy

Richard McGuire

Head Rates Strategy

+44 20 7664 9730

Richard.McGuire@Rabobank.com

Lyn Graham-Taylor

Senior Rates Strategist

+44 20 7664 9732

Lyn.Graham-Taylor@Rabobank.com

Credit Strategy & Regulation

Matt Cairns

Head Credit Strategy & Regulation

Covered Bonds, SSAs

+44 20 7664 9502

Matt.Cairns@Rabobank.com

Bas van Zanden

Senior Analyst Pension funds, Regulation

+31 30 712 1869

Bas.van.Zanden@Rabobank.com

Cas Bonsema

Senior Analyst Financials

+31 6 127 66 642

Cas.Bonsema@Rabobank.com

Maartje Schriever

Analyst ABS

+31 6 251 43 873

Maartje.Schriever@Rabobank.com

Agri Commodity Markets

Carlos Mera

Head of ACMR

+44 20 7664 9512

Carlos.Mera@Rabobank.com

Charles Hart

Senior Commodity Analyst

+44 20 7809 4245

Charles.Hart@Rabobank.com

Oran van Dort

Commodity Analyst

+31 6 423 80 964

Oran.van.Dort@Rabobank.com

Andrick Payen

RaboResearch Analyst

+1 212 808 6808

Andrick.Payen@Rabobank.com

Energy Markets

Joe DeLaura

Senior Energy Strategist

+1 212 916 7874

Joe.DeLaura@Rabobank.com

Florence Schmit

Energy Strategist

+44 20 7809 3832

Florence.Schmit@Rabobank.com

Disclaimer

Non Independent Research

This document is issued by Coöperatieve Rabobank U.A. incorporated in the Netherlands, trading as “Rabobank” (“Rabobank”) a cooperative with excluded liability. The liability of its members is limited. Authorised by De Nederlandsche Bank in the Netherlands and regulated by the Authoriteit Financiële Markten. Rabobank London Branch (RL) is authorised by De Nederlandsche Bank, the Netherlands and the Prudential Regulation Authority, and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Further details are available on request. RL is registered in England and Wales under Company no. FC 11780 and under Branch No. BR002630. This document is directed exclusively to Eligible Counterparties and Professional Clients. It is not directed at Retail Clients.

This document does not purport to be impartial research and has not been prepared in accordance with legal requirements designed to promote the independence of Investment Research and is not subject to any prohibition on dealing ahead of the dissemination of Investment Research. This document does NOT purport to be an impartial assessment of the value or prospects of its subject matter and it must not be relied upon by any recipient as an impartial assessment of the value or prospects of its subject matter. No reliance may be placed by a recipient on any representations or statements made outside this document (oral or written) by any person which state or imply (or may be reasonably viewed as stating or implying) any such impartiality.

This document is for information purposes only and is not, and should not be construed as, an offer or a commitment by RL or any of its affiliates to enter into a transaction. This document does not constitute investment advice and nor is any information provided intended to offer sufficient information such that is should be relied upon for the purposes of making a decision in relation to whether to acquire any financial products. The information and opinions contained in this document have been compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness.

The information contained in this document is not to be relied upon by the recipient as authoritative or taken in substitution for the exercise of judgement by any recipient. Any opinions, forecasts or estimates herein constitute a judgement of RL as at the date of this document, and there can be no assurance that future results or events will be consistent with any such opinions, forecasts or estimates. All opinions expressed in this document are subject to change without notice.

To the extent permitted by law, neither RL, nor other legal entities in the group to which it belongs accept any liability whatsoever for any direct or consequential loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

Insofar as permitted by applicable laws and regulations, RL or other legal entities in the group to which it belongs, their directors, officers and/or employees may have had or have a long or short position or act as a market maker and may have traded or acted as principal in the securities described within this document (or related investments) or may otherwise have conflicting interests. This may include hedging transactions carried out by RL or other legal entities in the group, and such hedging transactions may affect the value and/or liquidity of the securities described in this document. Further it may have or have had a relationship with or may provide or have provided corporate finance or other services to companies whose securities (or related investments) are described in this document.

Further, internal and external publications may have been issued prior to this publication where strategies may conflict according to market conditions at the time of each publication.

This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of RL. By accepting this document you agree to be bound by the foregoing restrictions. The distribution of this document in other jurisdictions may be restricted by law and recipients of this document should inform themselves about, and observe any such restrictions.

A summary of the methodology can be found on our website

© Rabobank London, 60 London Wall, London, EC2M 5AA +44(0) 207 809 3000